AI, Networks, and Verifications: Top Payments Leaders’ Predictions on Future Payments Technology

- 10 min read

Hear from Carey (Versapay) and Chip (Sage) on why:

- Business payment networks are set to boost connectivity and efficiency

- Artificial intelligence will bring predictive and proactive capabilities to the forefront, and

- Improved verification processes will ensure transactions are secure and seamless.

The world of payments is immensely novel, with a steady stream of disruptive innovations throwing an already progressive space into seemingly constant disarray. This is especially so for B2B enterprises, who despite transacting in massive volumes, are historically seen as payments laggards when compared to their B2C counterparts.

Yet despite adopting consumer-centric payments trends more slowly, the—not-so-distant— future of B2B payments looks remarkably transformative and prosperous. And businesses are rapidly understanding that unleashing working capital and satisfying their buyers hinges on how ahead they are of technological advancements in payments.

To make sense of the sweeping changes we might expect to see in payments technology in the coming years, we turned to two top payments leaders for guidance.

Carey O’Connor Kolaja, CEO at Versapay, and Chip Mahan, Global Commercial Head Fintech, Payments and Banking at Sage, understand better than most the consequential role payments play in accelerating cash flow and delivering exceptional value to customers. They’re also highly attuned to suppliers’ and buyers’ evolving needs and the ever-changing payments landscape.

Carey and Chip predict three major technology advancements will impact payments. These include: the ever-increasing value of business networks, the role of generative AI in business operations, and the need for continuous business identification and verification.

1. The ever-increasing value of business payment networks

The invoice to cash cycle is complex, complicated, and frankly, involves too much paper and manual intervention. Change is possible—and currently underway, with automation playing a significant role—yet true transformation requires greater collaboration between businesses.

A B2B payment network—that's integrated with multiple systems, like financial management solutions, banks, AP platforms, and ecommerce and POS solutions—can facilitate this change, and play an increasingly valuable role in the future.

Payments, as a sector, has always been—and will likely always be—about making payments and getting paid. But business networks—like Versapay’s—reimagine foundationally how businesses interact with one another, and Chip and Carey see their value growing exponentially in the coming years.

Modern finance, according to PYMNTS, is “No longer just about moving money. It’s about unlocking strategic value, fostering innovation, and reimagining business models.” And networks, that are deeply integrated with business processes and existing systems, do more than simply optimize buyer-supplier transactions. They stand to create value-added financial ecosystems that drive efficiencies through connectivity.

As Carey explains, "The value of the network, and networks in general, continues to be driving incredible value for the economy. And as we become more connected as a society; as we understand the context of what we need to do; as we think about democratizing access and movement of money, the network will ever be more prevalent. And that requires you to trust the people who are in your network, on your network, and who want to be part of the network."

While accounts receivable is well-positioned to benefit from the ‘network effect’, Chip reminds us that other finance departments will too profit. “You have your accounts payable, too, and your supplier information, and your customer information. So, having that entire data set within your network becomes a very powerful tool. As does how you use it to connect customers to customers, customers to suppliers, and suppliers to suppliers.”

The cost of capital is high, and payment fraud is surging. These days, companies are increasingly looking to established networks demonstrating secure and reliable transactions. Carey predicts that the future of mid-market business growth rests on technology partners that have proven confidence and fidelity in moving money.

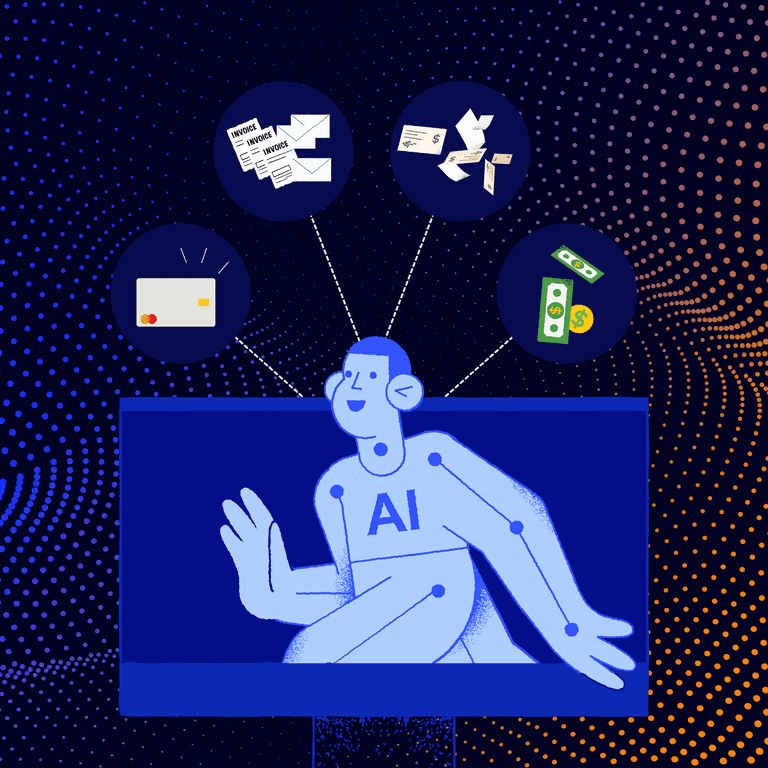

2. The role of generative AI in transforming payment operations

In a recent interview with Forbes, Jack Azagury, Group Chief Executive for Consulting at Accenture, said that generative AI is “the fastest growing technology we’ve seen in the history of our company.” While not necessarily the hottest take—considering how pervasive generative AI is right now—Carey and Chip suggest its use and prominence within—and influence over—payments will only grow.

According to Carey, "Generative AI has transformed the way we think about our day-to-day tasks, the information that we're able to get access to, the speed and efficiencies of which we're able to get jobs done, and the creativity that we could tap into that we never imagined.” These transformations will manifest—and in some cases, already are—across payments—and finance more broadly—in so many ways, including:

- Early issue detection: AI will identify potential problems (i.e., cash flow issues) before they become critical, allowing businesses to take preventive measures.

- Suggested solutions: AI will suggest and even automate solutions—to those AI-identified problems—such as applying on businesses’ behalf for pre-approved loans or adjusting payment terms with clients.

- Enhanced decision-making: By providing data-driven insights, AI will help businesses make informed decisions more quickly.

- Improved service: Proactive AI will anticipate customer needs and provide timely responses, enhancing customer satisfaction.

- Payment matching and reconciliation: AI engines will recognize characters on incoming payments receipts and remittance records, match them to outstanding invoices, apply cash, and generate accounting journal entries.

- Check processing (and subsequent digitization): AI will take manual payments, like checks, and using optical character recognition, ingest then digitize them, by converting text images into machine readable text formats.

Now, in no way is this meant to trivialize AI’s impact, but much of its imminent value and influence over payments will stem from the massive volumes of data it inevitably makes accessible, and more importantly, digestible. And with that data comes context.

As Carey explains: “This data will allow us to understand how we better serve our customers; what they need; how we anticipate what they don’t know are problems... Particularly when we think about cash flow, or we think about payment choices.”

What she makes clear, is that data and customer-centricity are linked; and AI has the potential to be the glue that inextricably binds them.

Perhaps not surprisingly, this sentiment is not lost on executives. In fact, a recent study of ours found that 92% of leaders agree that reaching peak performance depends on all departments within their organization being digitized. And what better way to envision these AI-driven transformations in payments than through a real-world example?

Sage recently unveiled their ‘Copilot’, a dedicated, AI-powered productivity assistant. According to Chip, it’s a perfect companion for businesses wanting “proactive responses that they can deliver to customers for problems they don’t even know about.”

And if you remember our callout just above about AI suggesting solutions? Well, Chip elaborates with an example:

“If I’m a customer of ours, and I log into my Sage network, I might immediately be told 'You're going to have a cash flow problem in six weeks from now, and I’m going to let your accountant—your trusted advisor—know about that as well’. That’s great, but generative AI can take this even further and suggest solutions. Imagine the software then telling me that I'm eligible for various loans and am already pre-approved and asking whether I’d like to move forward. This technology is providing solutions for problems our AI is recognizing, and not simply surfacing the problems alone. And that’s just how fast it’s moving today.”

3. Continuous business identification and customer verification

A sizeable percentage of mid-market businesses currently rely on manually processes for identifying and verifying both businesses and transactions, which are time-consuming and prone to errors. (Not to mention typically needing extensive paperwork.)

Most associate this practice with B2C, as it tends to involve businesses collecting personal details from customers and then comparing those against official records or documents. For instance, identification such as passports or driver's licences are checked against public records and credit reports; other identification confirmations include requests for names, birth dates, addresses or phone numbers. This is primarily in service of businesses verifying that their customers are who they claim to be, so that service isn’t slowed down, and businesses are guarded against fraud and comply with legal requirements.

Regarding payments, real-time verifications are most common, as they’re instantaneous and typically take place when conducting transactions—like through an ecommerce checkout.

But as Carey suggests, “It’s happening in the business space, too.” Yet right now, unlike B2C, it’s really hard for businesses to do business with each other. Plus, she explains, “It’s an area that hasn’t really been totally disrupted over the last couple decades.”

Businesses selling to businesses care about customer identity verifications as much as businesses selling to consumers. They want to comply with regulations; they want to prevent fraud; they want better security; they want to deliver improved customer experiences; and they want to prosper. It’s just not that easy currently.

Carey explains that “[B2B] businesses tend to have to pull a lot of paper and information to verify not just that the business exists, but that the individuals and beneficiaries of those businesses are associated with them, and that they can act on behalf of the business, to even move money and pay invoices.”

But Carey suggests that this is an area where major transformation is soon set to materialize. She is seeing a lot of—and expects to see more—grassroots movements and companies trying to transform business identification and verification.

“And when we do that, and particularly when we work with partners that can help us do that, it removes friction from the system, whether it's a one-time payment or being able to do business with a number of different partners.”

Business buyers are sophisticated, and they expect payment processes to be quick, easy, and dare I say it, enjoyable. Yet with growing expectations, and an increasing awareness of data privacy issues, comes the need for greater transparency and control over data. Carey’s prediction recognizes this and highlights how important an efficient and accurate verification process is to ensuring smooth transactions.

Embrace the future of payments technology

As Carey so tidily puts it, “The future has already happened, you just haven’t seen it yet”. B2B payments is at an exciting juncture, and three game-changing advancements are forcing and fuelling its evolution: the growing importance of business networks, the transformative power of generative AI, and the critical need for continuous business identification and verification.

Business networks are set to boost connectivity and efficiency; artificial intelligence will bring predictive and proactive capabilities to the forefront; and improved verification processes will ensure transactions are secure and seamless.

For businesses selling to businesses, the message is clear: now is the time to embrace these technological payments advancements. But tapping into robust payment networks, using AI for smarter decision-making, and adopting advanced verification methods, companies can streamline their financial operations, cut down on fraud, and offer top-notch customer experiences. Embracing these innovations will drive growth and keep you ahead of an ever-changing payments landscape.

About the author

Jordan Zenko

Jordan Zenko is the Senior Content Marketing Manager at Versapay. A self-proclaimed storyteller, he authors in-depth content that educates and inspires accounts receivable and finance professionals on ways to transform their businesses. Jordan's leap to fintech comes after 5 years in business intelligence and data analytics.

Digital Payments

All you need to know to make the switch to digital payments.

Always stay up-to-date

Subscribe

Join the 50,000 accounts receivable professionals already getting our insights, best practices, and stories every month.